Emerald Pages

◆

Photo: U.S. Money Reserve

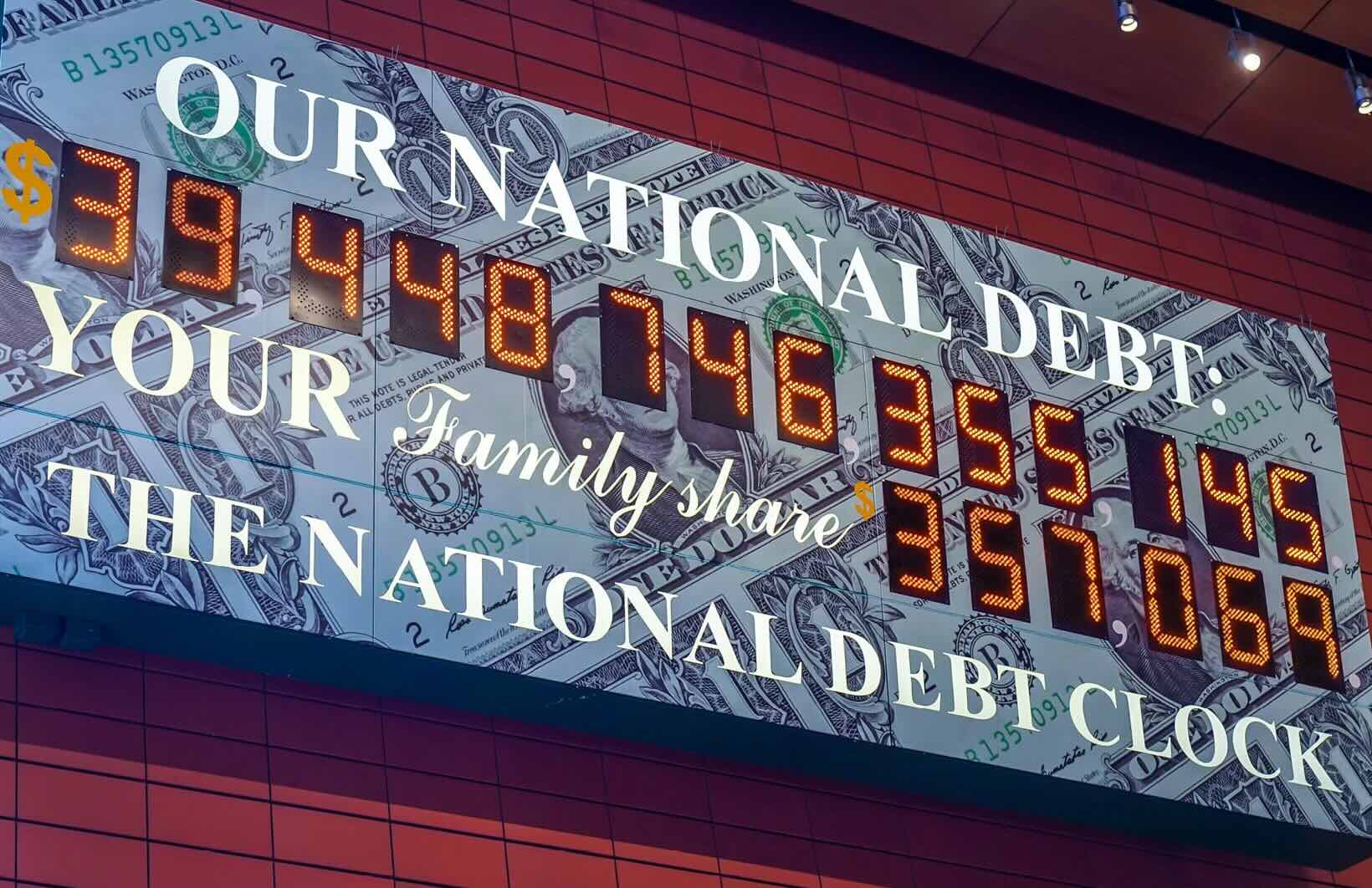

In July 2006, the gross national debt of the United States stood at roughly $8.45 trillion. Twenty years later, in July 2026, that number has climbed to a staggering $39.4 trillion—an exponential surge of roughly 366%. This $30.94 trillion increase over two decades represents more than just a number on a ledger. It is the engine driving a dangerous inflationary cycle that is quietly eroding the purchasing power of every American, forcing families into a desperate reliance on credit just to afford basic necessities.

While headline inflation has recently cooled to 3.5% in June 2026, this reprieve is temporary. The underlying structural pressures—massive deficit spending, rising interest rates, and a debt-to-GDP ratio that has ballooned from 64% to 131%—remain firmly in place. What is unfolding is a debt-fueled inflationary trap, a vicious cycle where the cost of living outpaces wages, people turn to credit to survive, and that very credit keeps prices artificially high, worsening the inflation they are trying to escape.

The past two decades have been punctuated by key catalysts that accelerated this debt surge. The 2008 Financial Crisis triggered massive bank bailouts, quantitative easing, and the American Recovery and Reinvestment Act, adding trillions to stimulate a collapsing economy. The 2020 COVID-19 pandemic then forced an unprecedented $4.5 trillion in emergency relief spending in a single year. Compounding these crises are persistent structural deficits—ongoing tax cuts paired with mandatory entitlement programs like Social Security and Medicare that consistently outpace federal revenue collections.

How Government Debt Drives Inflation

The connection between government debt and inflation is not always direct, but the mechanisms are well understood. When the government spends more than it collects in taxes, it borrows to bridge the gap. This deficit spending injects artificial demand into the economy—cash is pushed directly into the hands of consumers and businesses. If the supply of goods cannot keep up with this new demand, prices inevitably rise.

Additionally, when the Federal Reserve buys government bonds to keep interest rates low, it pays for them by creating new bank reserves, effectively increasing the money supply. More dollars chasing the same amount of goods lowers the purchasing power of each dollar. This is the "inflation tax"—a temptation for highly indebted governments to tolerate higher inflation, allowing them to repay fixed-rate debts with future dollars worth significantly less than when they were originally borrowed.

- Debt-to-GDP Ratio: Surged from ~64% in 2006 to ~131% in 2026, signaling that debt is growing faster than the economy can support.

- Debt Per Citizen: Rose from ~$28,000 to ~$115,188—an $87,188 increase per person in just 20 years.

- Interest Payments: Annualized interest on the debt alone has surpassed $1 trillion, self-compounding the deficit.

The Consumer Debt Feedback Loop

As government debt fuels inflation, the pressure trickles down to household budgets. With wages failing to keep pace with rising prices, families are increasingly forced to rely on credit cards, personal loans, and "Buy Now, Pay Later" services just to cover everyday essentials like groceries, utilities, and rent. This is where the vicious cycle tightens.

Consumer debt contributes to inflation by accelerating current demand through future income. When people use credit to buy goods today, they inject immediate purchasing power into the economy. Retailers see that demand remains high, so they have no incentive to lower prices. Prices remain sticky, and consumers are forced to borrow even more the following month. What begins as a survival mechanism inadvertently backfires, keeping inflation elevated and intensifying the very financial strain it was meant to alleviate.

This cycle cannot continue indefinitely. The Federal Reserve, recognizing the danger, has kept interest rates elevated—with newly appointed Fed Chairman Kevin Warsh stating the central bank has "no tolerance" for elevated inflation. High interest rates make the credit cards and loans people are using to buy food drastically more expensive, creating a second mountain of personal debt. Eventually, consumers hit their maximum credit limits, and a massive amount of household income is redirected away from the economy and sent directly to banks to pay off interest, threatening to trigger a sharp economic slowdown.

The Trump Administration's Role

Critics and nonpartisan economists point to the current administration's policies as a primary accelerant of this debt-inflation spiral. The economic agenda centered on aggressive import tariffs, major deficit-financed tax cuts, and geopolitical friction is compounding financial pressures on households.

The direct inflationary impact of tariffs functions as a consumption tax on imported goods. Studies by the Yale Budget Lab estimate that these broad import penalties cost the average U.S. household roughly $1,700 annually in higher prices. Meanwhile, deficit-financed tax cuts—particularly the extension of the "One Big Beautiful Bill" business tax provisions—are projected by the Committee for a Responsible Federal Budget to add an estimated $5 trillion to the debt over the next decade. This fiscal expansion, coupled with military friction with Iran, has sent benchmark 10-year Treasury yields climbing above 4.4%, further ballooning the cost of servicing the national debt.

A Disproportionate Burden on Black America

The intersection of macro debt, inflation, and current policy has created what civil rights organizations are calling a disproportionate economic crisis for Black Americans. Research from the Joint Center for Political and Economic Studies and the National Urban League reports that a "Black recession" began taking hold in 2025 and continues into 2026.

The vulnerabilities are stark. The administration's aggressive federal workforce downsizing has resulted in the loss of roughly 277,000 civil service jobs, disproportionately affecting Black professionals who have historically relied on the federal government as a primary vehicle for middle-class economic mobility. Manufacturing and supply chain disruption from tariffs has caused a contraction of 72,000 jobs in sectors where Black workers over-index. Consequently, the Black unemployment rate surged to 8.2% in late 2025 and remains highly elevated in 2026, resting at more than double the unemployment rate of white Americans.

Additionally, because lower-income households spend a significantly higher percentage of their take-home pay on immediate necessities, tariffs and inflation function as a regressive tax. To offset the rising national debt and fund the administration's $5 trillion tax cuts, the 2025 "Megabill" legislation enacted deep cuts to social safety nets—reducing funding for SNAP (food assistance) and Medicaid, programs that millions of working-class Black families rely on to bridge economic gaps.

Black entrepreneurs face a compounding crisis as well. Inflation on raw materials, combined with tariff-induced tech and equipment price hikes, has squeezed small enterprises. Meanwhile, executive actions have defunded the Treasury's Community Development Financial Institution (CDFI) fund and moved to dismantle the Minority Business Development Agency (MBDA), threatening an estimated $10 billion to $15 billion in capital and support earmarked for minority firms.

Breaking the Cycle: Pathways Forward

To break this cycle, solutions must target both national economic policy and personal financial strategies. At the macro level, rolling back broad tariffs in favor of targeted trade agreements to instantly lower the cost of raw materials and consumer goods. Fiscal deficit reduction—balancing government spending with revenue generation—would reduce artificial demand pumped into the economy, allowing the Federal Reserve to safely lower interest rates. Re-strengthening agencies like the Consumer Financial Protection Bureau (CFPB) would ensure strict oversight of predatory lending and hidden fees that drain household wealth.

At the personal level, families caught in the trap of using debt to pay bills can take aggressive steps to stop the bleeding. Switching to cash or debit for immediate necessities prevents credit card interest from compounding on consumable items. Negotiating with utility and internet providers for hardship programs, exploring 0% APR balance transfer cards, and utilizing Community Development Financial Institutions (CDFIs) for safer, lower-interest small-dollar loans can provide relief.

The path out of this crisis requires both immediate relief and long-term structural reform. Without it, the vicious cycle of debt and inflation will continue to tighten its grip—not just on the national balance sheet, but on the daily lives and economic futures of everyday Americans.

No Ads. By Us. For Us.

This article was made possible by readers like you. We hope it inspired you to support Emerald Book, so we can continue producing content like this.

We will never show you ads, sell your data, or require a subscription to consume our content. Your gift helps us keep the truth accessible.

Click the Support button to give a gift of any amount today.

Thank you for making this work possible.